How might lower inflation affect your investments?

The latest figures show that inflation continues to fall, with consumer prices rising just 3.2% in the year to March 2024. This is the lowest rate for more than two years, and will be welcome news for most. What’s more, many will be hopeful that interest rate cuts will follow suit and lead to lower borrowing rates.

While the latest CPI inflation rate is higher than the expected 3.1%, it is well below the 10.1% recorded by the Office for National Statistics in March 2023. Lower food inflation is one driver. (Down to 4%, from 19.1% last year.) Prices for some products, including cheese, meat and household goods, have even fallen. However, petrol and diesel prices rose.

In this article, we consider what the changing climate means for your investments, and how to adjust strategies to deliver the best possible returns.

When will interest rates go down?

The Bank of England and other forecasters expect price rises to continue to slow, and inflation to return to more normal rates, of around 2%, by the end of 2025. Nonetheless, interest rate reductions may be slow in coming, having remained at a 15-year high of 5.25% since August last year. The markets had been anticipating a series of interest rates cut this year, but few experts now expect any reduction before August or September. Tensions in the Middle East and the situation in Ukraine, and the impact on fuel prices, will be a factor.

‘As a result of inflation remaining sticky, particularly in the US, the signals from central banks are that interest rates may remain higher for longer,’ says Paul Willans, Managing Director of AJB Wealth in Hampshire. ‘But it’s possible that interest rates in the UK and Europe will fall sooner than in the US.

‘In addition, you have to bear in mind that world economies such as the US are performing better than anticipated. This has helped the US avoid recession to date and has proved positive for stock markets in the year to date.’

Adjusting investment strategies

AJB Wealth manages investment portfolios for both local and overseas clients from its base near Winchester in Hampshire.

‘Inflation has a profound impact on investments,’ says Willans, a chartered wealth manager. ‘In periods of high inflation, investors try to protect portfolio values by holding assets that tend to perform well in that environment.

‘Tactical investors have been employing different strategies for some months, with bonds playing a more important part in portfolios. This will be particularly true if lower inflation comes hand in hand with slowing economic growth.’

Impact of lower inflation on investments

1. Fixed-income securities: Bonds

Lower inflation is linked to lower interest rates, as the Bank of England and other central banks ease controls on the availability of money to maintain economic growth, by lowering interest rates. This increases the appeal of higher-yielding assets, such as gilts and bonds, and the price that investors will pay for them.

When purchasing an existing bond, an investor is buying the right to a future income and will accept a yield that is competitive against prevailing interest rates. This means that existing bond owner can demand a higher price for their bonds.

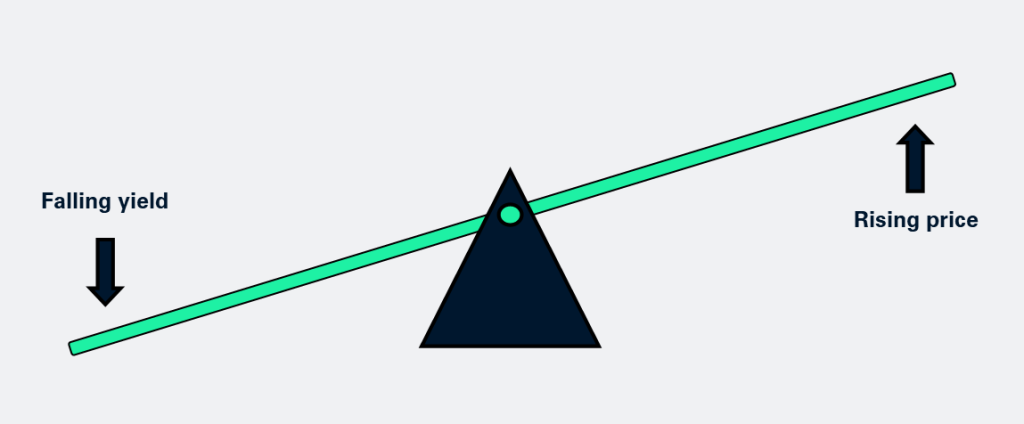

Of course, as we have experienced in recent years, the reverse is true and, in a rising interest rate environment, the capital value of bonds falls. Put simply, it’s like a seesaw.

As inflation continues to fall, the holders of bonds should see the value of their assets rise. Bonds also provide certainty. This is especially important if economic growth stalls, meaning equity prices and dividends are likely to suffer. UK GDP grew by just 0.1 per cent last year, though it is forecast to grow by 0.8% in 2024 and 1.9% in 2025, according to the Office for Budget Responsibility (OBR).

The desirability of bonds will depend on where we are in the cycle, and what we want to achieve in terms of capital growth, income and certainty.

2. Equities

Historically, shares have performed well when inflation is low, but this is a generalisation, with many factors at play – particularly economic growth. Different types of companies and sectors will be affected differently.

Generally speaking, low inflation is linked to higher spending and greater confidence amongst both consumers and businesses. As companies may have increasing sales, but do not have steeply rising costs, they may be able to improve profit margins. This may lead to larger dividends and higher share prices.

Growing companies in particular may benefit most from lower inflation as lower interest rates make it cheaper to borrow money. Particular sectors that seem to thrive in lower inflation conditions include technology and healthcare.

The rate of falling inflation, relative to other countries, will also impact on currency exchange rates. This can impact on whether exported goods and services will become more or less competitive.

Investment strategies for lower inflation

1. Diversification

Diversifying across, and within, asset classes is considered a fundamental strategy for managing risk. This can help mitigate volatility and enhance returns.

Within fixed interest, this can mean buying bond with a short-life (or ‘duration’) while interest rates are rising, in order to mitigate capital loss, but switching to longer-duration bonds, when interest rates are falling.

2. Risk management

Periods of lower inflation can create a false sense of security, leading investors to underestimate risks. It’s important to ensure that a thorough risk assessment is done, taking into account factors such as market volatility, geopolitical events, and changes in interest rates. Your wealth manager will assess both your attitude to risk, and your capacity to take risk.

3. Regular portfolio reviews

‘Whoever is managing your investment portfolio, it’s vital that it is reviewed on a regular basis,’ says Willans. ‘Not only do market conditions and economic factors change, but your own personal circumstances and goals may evolve. AJB Wealth can review your portfolio and formulate a robust plan taking into account both the economic environment and your personal situation.’

Conclusion

Changing economic environments offer both challenges and opportunities. By understanding the impact of declining inflation on different asset classes, it is possible to make strategic adjustments and get into position for financial success. AJB Wealth has the knowledge and tools to help clients make the most of their assets.

‘As active managers, we can be nimble and adapt to short-term opportunities, rather than just hoping that it’ll turn out alright in the long run,’ says Willans.

To discuss your own situation, please speak to us. Our experienced and highly-qualified team at AJB Wealth can work with you to help you achieve financial efficiency and security. To arrange an initial consultation, book a meeting, or call us on 01483 774 070.

Important: The content of this bulletin is for general consideration only and does not constitute advice. No action must be taken, or refrained from being taken, without first seeking appropriate advice. This company accepts no responsibility for any loss occasioned as a result of any such action, or inaction. It’s important to remember that investments can fall, as well as rise. In the event of early encashment, you may receive less back than your original investment.