What are ETFs and why do we use them?

Low cost and efficient, it’s no wonder that exchange-traded funds (ETFs) have become a key investment tool since they were first developed in the 1990s. In June 2023, assets invested in global ETFs hit a record high of $10.3trn.

Like other collective funds, an ETF is a basket of shares, bonds or other assets. However, they have advantages over other funds that make them appealing to many types of investors.

‘ETFs are a core element of our investment strategy at AJB Wealth,’ says Managing Director Paul Willans. ‘They not only allow us to react swiftly and tactically to market changes, but enable us to track indices very efficiently. All while keeping costs firmly under control.’

In this article, we explore the benefits of ETFs, and go on to explain the difference between physical and synthetic ETFs.

1. ETFs are easy to trade

Unlike other funds, an ETF can be bought and sold on listed stock exchanges. While most collective funds trade only once a day, an ETF can be traded at any time an exchange is open. This provides a huge advantage over collective funds. Not only do investors have more flexibility, but they know the trade price at the time of placing an order to buy or sell.

2. An efficient way to diversify

An ETF is a cost-effective way of achieving the best mix of investments. They typically track an index, such as the FTSE 100 or S&P 500, or a particular sector, commodity or other asset. In fact, they can be used to gain exposure to almost any asset class or sector.

There are even cryptocurrency ETFs, which seem set to become all the rage. Sustainable ETFs – where environmental, social and governance factors are taken into account – are another growth area.

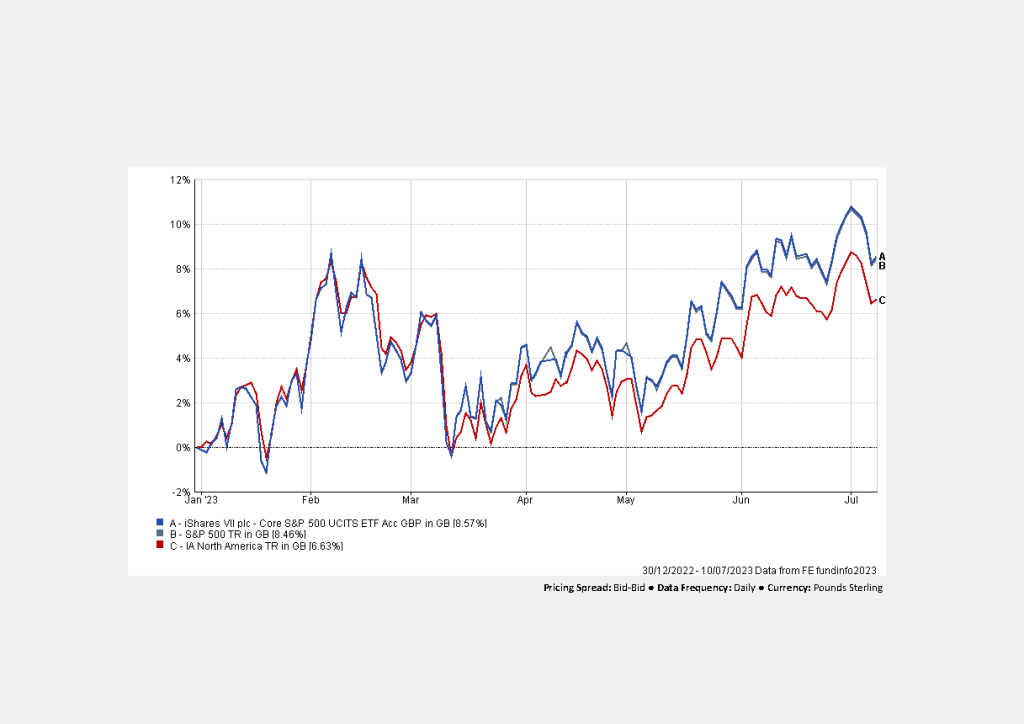

‘Whereas few active managers outperform the market, ETFs are designed to accurately track their index. And as you can see from the chart below, they track like a shadow,’ says Willans.

Beyond that, there is enormous flexibility in how ETFs are structured, so they can be used to follow specific investment strategies.

The graph below shows one of the largest ETFs that tracks the S&P 500 Index (an index of the largest companies, by capitalisation, in the USA), over the current year to date. The blue line (A) is the ETF; the green (B) is the S&P 500 index itself, while the red line (C) represents the average UK fund investing in North American equities.

3. ETFs are low cost

Due to their structure, ETFs are generally cheaper to run than most funds. They usually, but not always, have lower charges. Most index tracking ETFs typically have no upfront charge and their ongoing fees can be below 0.10% pa. Whereas a collective fund may have upfront charges plus an ongoing fee of 1-1.5% pa.

‘The combination of market certainty and low charges are why they have become invaluable additions to actively-managed portfolios,’ says Willans.

4. Sophisticated trading options

ETFs allow for sophisticated risk management strategies through ‘hedging‘ – a way to limit losses or protect future prices. Most ETFs allow hedging in various currencies. So, if a UK investor wants to invest in US equities, but is worried that the Dollar may fall against Sterling, they can hedge their exposure and remove that specific risk. Of course, if they think that the Dollar will rise against Sterling, they might opt to be exposed to the currency risk.

5. Greater transparency

Collective funds are only required to publish details of their holdings twice a year in the UK. By comparison, ETFs usually publish their holdings daily. This means that investors know which securities are held and whether the fund remains in line with their investment aims.

Types of ETF

There are two types of ETF: physical and synthetic.

Physical ETFs

Physical ETFs invest directly in the underlying assets. In the case of a FTSE 100 tracker, the ETF invests in the shares of the index’s constituent companies. Meanwhile, a gold ETF owns actual gold bullion. However, it’s important to note that when you invest in an ETF, you buy a stake in the ETF itself, not the index being tracked or the underlying investment.

Synthetic ETFs

Synthetic ETFs are more complex. They purchase ‘derivatives’, rather than shares. Synthetic ETFs promise to match the same returns as the index or underlying investment they track. They enable investment in hard-to-access markets, such as those for perishable commodities or stock markets that restrict foreign investment.

They are considered riskier than physical ETFs due to what’s known as ‘counterparty risk’. This means that, if the investment bank that has sold the swap to the ETF can’t meet its obligations, you could lose your money. Sellers of swap contracts (where the parties agree to exchange cash flows or liabilities) usually have to provide collateral to reduce this risk, and investment managers are expected to undertake due diligence on this risk. Bear in mind though, that many collective funds are also exposed to counterparty risks.

In conclusion

The core difference between ETFs and other collective funds is that they can be traded on a listed stock exchange. This gives the investor greater control and flexibility. The most obvious advantage for many is the low costs associated with ETFs, while transparency is a key element for others.

At AJB Wealth, our experienced and highly-qualified team is well placed to work with you, and your other professional advisers, to help you achieve financial efficiency and security. To arrange an initial consultation, please book a meeting, or call us on 01483 774 070.

Important: The content of this bulletin is for general consideration only, and does not constitute advice. No action must be taken, or refrained from being taken, without advice. This company accepts no responsibility for any loss occasioned as a result of any such action, or inaction. You are also reminded that investments can fall, as well as rise, and, in the event of early encashment, you may receive less back than your original investment. Where overseas investments are held the rate of currency exchange may also cause the value of such investments to fluctuate.